By Sara Loo, Associate Research Officer at ISEAS-Yusof Ishak Institute

Malaysia aspires to become a leading digital economy, and data centres have been placed at the heart of this vision. Between 2021 and 2024, the country attracted MYR 184.7 billion (USD 43.7 billion) in data centre-related investments as part of its broader strategy to drive digital infrastructure development.

Data centres—physical facilities that house computer systems, servers, and storage—are critical to storing and processing the vast volumes of data required in the digital age. They are also foundational to the computational power needed for large-scale artificial intelligence (AI) applications.

As of December 2024, 38 data centre projects in Malaysia have secured Electricity Supply Agreements (ESAs), with a total maximum demand of 5.9 GW and an actual load utilisation of 405 MW. Although this current utilisation represents only about 3% of Tenaga Nasional Berhad’s (TNB) total contracted capacity of 13.76 GW, the projected maximum demand from these projects alone accounts for nearly 43%* of TNB’s total supply—a striking figure that raises important concerns.

While the ramp-up in energy usage is expected to be phased, the scale of Malaysia’s commitments calls for scrutiny. Has the country overcommitted to data centre development without proportionate investments in its energy capacity and infrastructure? This piece examines Malaysia’s current policy approach to balancing digital growth with energy sustainability.

Data Centre Growth and Rising Energy Demand

Malaysia’s data centres are primarily concentrated in two regions: Johor, at the southern tip of Peninsular Malaysia bordering Singapore, and Klang Valley, which encompasses Kuala Lumpur, Port Klang, and Cyberjaya.

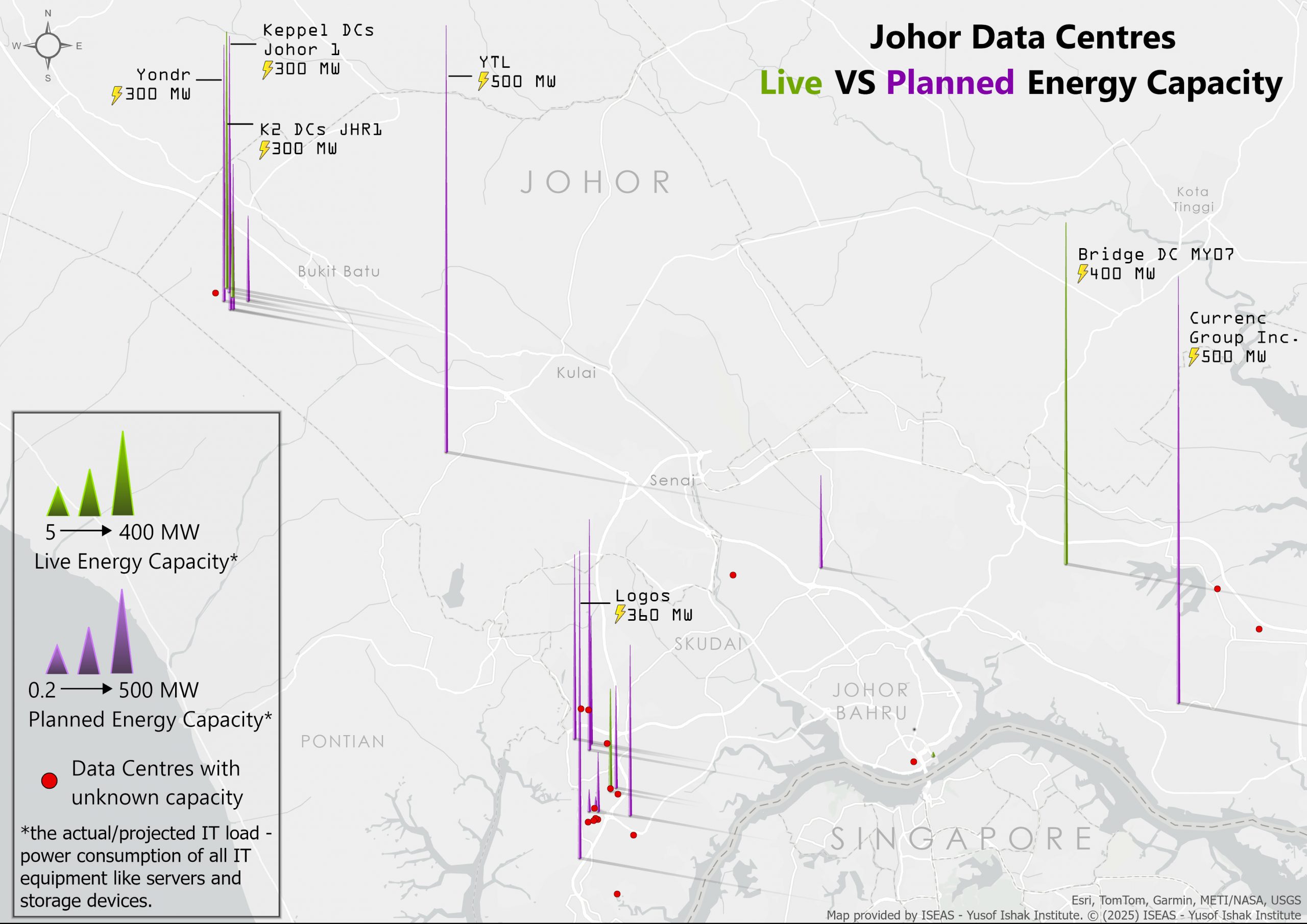

Johor, in particular, has emerged as the fastest-growing data centre market in Southeast Asia. The state’s data centre capacity surged from 10 megawatts (MW) in early 2021 to approximately 1.3 gigawatts (GW) by November 2024. This figure is projected to more than double, reaching 2.7 GW by 2027.

Source: Author’s compilation

Rising Electricity Prices: A Potential Consequence of Data Centre Expansion

One notable concern surrounding the rapid expansion of data centres is the potential impact on electricity prices. In more mature data centre markets, such as the state of Georgia in the United States, the influx of data centre investments has been linked to rising energy costs for residents and small businesses. Since 2023, the average Georgia Power residential customer has seen monthly electricity bills increase by USD 43, prompting the introduction of a Senate Bill to address the issue.

Similar concerns are emerging in Malaysia. Following Tenaga Nasional Berhad’s (TNB) announcement in December 2024 of a proposed 14.2% increase in base electricity tariffs starting July 2025, questions have been raised about the drivers of rising energy costs. Higher fuel costs are assumed to be the primary driver, alongside operational, maintenance, and grid enhancement expenses.

Some of these higher expenditures may be partially attributed to the growing number of data centres, which require continuous 24/7 electricity and place significant strain on the energy infrastructure.

Current Policy Approach

Malaysia addresses the increasing energy demands of data centres by focusing on two main strategies to lessen environmental impact, which are boosting energy efficiency and expanding renewable energy use. This dual approach is based on the conviction that optimising Power Usage Effectiveness (PUE) and similar metrics, combined with a shift to cleaner energy, will adequately support the sector’s sustainable expansion.

The latest policy update recommends that hyperscale data centres—defined as those with a capacity exceeding 21 MW—achieve a PUE of 1.4 or lower in order to be eligible for tax incentives. In practice, this means that if a data centre’s planned IT load is 400 MW (such as Bridge DC MY07, illustrated in Figure 1), the total facility’s power consumption should ideally not exceed 560 MW (400 MW × 1.4).

Sustainable Development Guidelines: Are They Enough?

While recent guidelines provide incentives to optimise PUE, they remain non-binding and serve only as recommendations. Key documents include the Johor state planning guidelines for data centres, MIDA’s guideline for sustainable development of data centres —which outlines eligibility for tax incentives under the Digital Ecosystem Acceleration (DESAC) scheme, and the latest policy update from the Ministry of Investment, Trade and Industry (MITI).

Across these documents, most provisions are framed as suggestions rather than enforceable requirements. For instance, the recommendation to adopt renewable and energy-efficient technologies lacks clear regulatory backing. Moreover, the guidelines do not specify expected targets for carbon emissions reduction through such technologies, whether via energy-efficient hardware, AI-optimised cooling systems, or improved data centre design and operations.

Next, conversations with policymakers in the AI ecosystem and Johor regional investment offices suggest that Malaysia is only “just starting to research the carbon emissions produced by data centre developments.” One policymaker acknowledged the high associated energy costs but admitted that they “haven’t come to a landing yet on what the next narrative would be on those kinds of conversations.”

Solar Power: A Limited Solution

While solar energy holds promise, its potential for powering data centres should not be overstated.

First, the intermittent nature of solar energy—combined with underdeveloped battery storage—makes it unreliable for data centres, which require 24/7 power. Due to limited solar generation capacity, many data centres in Malaysia still rely on diesel backup generators.

Second, land requirements are substantial. On average, 10 acres are needed to produce 1 MW of electricity. To meet the projected 5.9 GW demand from 38 data centre projects with Energy Supply Agreements (ESAs), about 59,000 acres of solar panels would be needed—over 60% of Johor’s 96,680-acre landmass. Rooftop solar helps but contributes minimally. For example, AirTrunk’s 150 MW JHB1 hyperscale facility in Johor generates only 1 MW from its solar-ready roof—just 2% of its current phase’s energy needs.

Moreover, Malaysia’s power grid remains carbon-intensive. In 2023, only 8.3% of Tenaga Nasional Berhad’s (TNB) electricity came from renewables; the majority came from coal and gas.

Finally, cost is another constraint. Industry players cite higher costs for renewables versus grid electricity, partly due to the System Access Charge (SAC) imposed by the Energy Commission. Intermittent generators face a higher SAC (45 sen/kWh) compared to those supplying firm power (25 sen/kWh).

Conclusion

Malaysia’s data centre boom underscores its digital ambitions, but sustaining this growth requires urgent attention to energy demands and environmental impacts. Current incentive-based policies are insufficient. To ensure long-term resilience, Malaysia must adopt enforceable regulations that require data centres to shoulder their fair share of energy infrastructure costs—without burdening households or small businesses.

Balancing digital growth with sustainability is not just desirable; it is essential for Malaysia to truly become a digital powerhouse.

Note: The 43% figure is derived by dividing the reported maximum demand of 5.9 GW (as referenced in TNB’s Q4 FY2024 Analyst Briefing) by TNB’s total contracted capacity of 13.76 GW, as stated on its website.

About the Writer

Sara Loo is Associate Research Officer with the Malaysia Studies Programme at the ISEAS-Yusof Ishak Institute. She has published works about Malaysia’s green economy, including a monograph on Malaysia’s emerging electric motorcycle sector. Her policy pieces have been published by the institute’s commentary site Fulcrum and the South China Morning Post.

The views and recommendations expressed in this article are solely of the author and do not necessarily reflect the views and position of the Tech for Good Institute.

This article is based on the original piece published by the ISEAS Yusok Ishak Institute on 12 June 2025.